PSD2 and Strong Customer Authentication (SCA)

Payment Services Directive II (PSD2) revised the first Payment Services Directive, regulating all payment services across the European Union (EU), the European Economic Area (EEA) and the United Kingdom. It became effective in January 2018 to create a more open, competitive payments landscape across Europe. The revised directive introduced Strong Customer Authentication (SCA)—a set of requirements for authenticating online payments—became enforceable in 2021 across the EEA region and in March 2022 in the UK.

SCA ascertains a customer's identity and relies on the presence of at least two factors for authentication of a transaction. Transactions that are not authenticated might be declined.

The impact of PSD2

All online businesses accepting credit card payments need to make sure their checkouts can perform SCA challenges so that card-issuing banks can process payments unless an exception under the SCA rules would apply. If the required level of authentication is not provided, transactions will be declined.

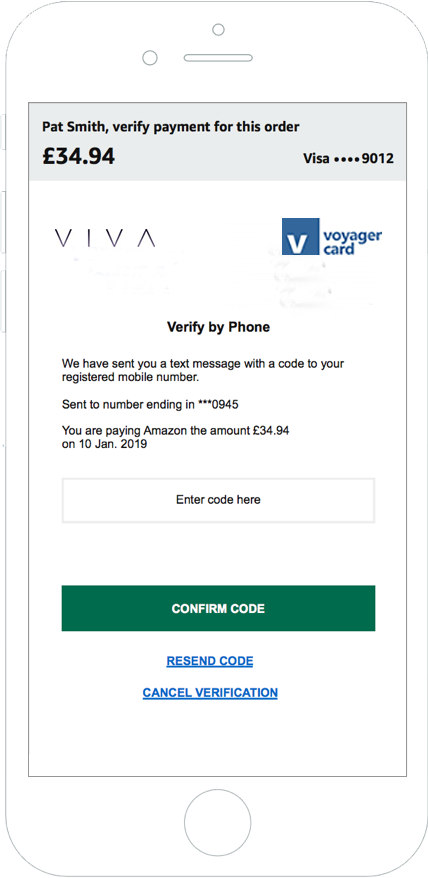

Card-issuing banks who use authentication services offered through Visa or MasterCard display a challenge screen similar to the one below when customers place orders using their credit card.

When selling online, it’s important for you to help educate your customers about SCA and what they should do when they see a SCA challenge to avoid cart abandonments.

SCA and your Amazon Pay integration

To make sure your Amazon Pay integration supports SCA, refer to the table below:

|

Custom integrations |

Ecommerce solutions |

|

If you use a custom Amazon Pay integration, make sure your implementation uses Amazon Pay Checkout v2. |

If you’ve used an off-the-shelf ecommerce solution to add Amazon Pay to your store, make sure to use the corresponding plugin or online store system that supports Amazon Pay Checkout v2. |

For more information, contact your Account Manager or Amazon Pay merchant support.