Note To prevent abandoned carts and to continue offering your buyers a seamless checkout experience under the second Payment Services Directive (PSD2), we recommend to update your Amazon Pay integration as described under Upgrading your Amazon Pay integration for PSD2. Only use the fallback solution if no update is available for your online store.

SCA fallback solution for your Amazon Pay integration

In line with the second Payment Services Directive (PSD2), we have launched functionality that enables authentication challenges for buyers. To fully benefit from this functionality, you can be required to update your Amazon Pay integration.

If strong customer authentication (SCA) is enforced and you haven’t updated your Amazon Pay integration, your integration automatically switches to the fallback solution that meets PSD2 requirements for SCA. The fallback solution doesn’t offer the seamless user experience that a fully upgraded integration provides.

The fallback checkout flow differs depending on the payment authorisation model your Amazon Pay integration uses. In general, the Amazon Pay checkout uses one of two models – buyer present (synchronous authorisation) and buyer not present (asynchronous authorisation).

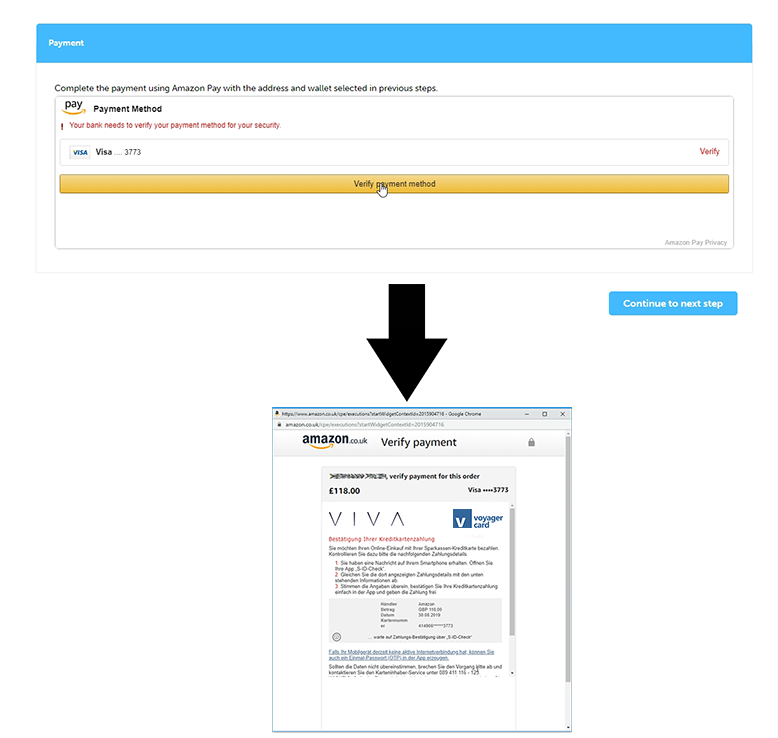

Fallback flow for synchronous authorisations

In the fallback flow for synchronous authorisation buyers will have to click an additional button before they’re forwarded to the page where they can complete verification.

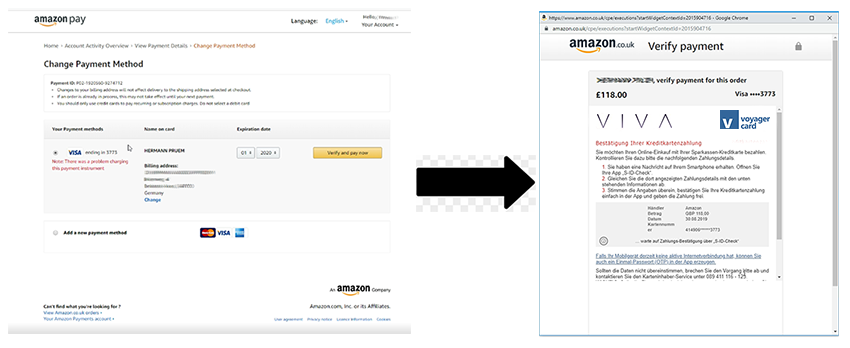

Fallback flow for asynchronous authorisations

The fallback flow for asynchronous authorisations will prompt customers to sign in to their Amazon account to complete the verification challenge there.

To prevent abandoned carts and allow for a seamless authentication flow during checkout, Amazon Pay recommends to upgrade your integration as soon as possible. For detailed information on how to upgrade, see Upgrading your Amazon Pay integration for PSD2.

If unsure, which authorisation model you use, here’s a very high-level definition: Amazon Pay integrations that use synchronous authorization, authorise payments upon every order that is processed. Amazon Pay integrations that use asynchronous authorisation never authorise the payment immediately after the order was placed.

If your integration doesn’t support decline handling as recommended by Amazon Pay, your online store will not show the fallback solution described above. Integrations without decline handling will not support SCA challenges. For more details about decline handling, see the integration guide.